Introduction

Fraud is no longer a back-office problem, it’s a boardroom priority.

As financial crime grows more sophisticated, so does the technology built to stop it. From AI-generated deepfakes bypassing biometric checks to synthetic identities slipping through onboarding flows, the fraud landscape in 2025 demands smarter, faster, and more layered defenses than ever before.

Yet for every CISO, compliance head, risk officer, and developer trying to build the right stack, the same questions keep coming up. What actually works? How do fraud detection services differ from fraud prevention solutions? When does a KYB solution become necessary? How do deepfake detection solutions fit into a KYC workflow? And what does a genuinely ROI-positive fraud prevention and AML compliance program look like in practice?

We compiled the 50 most searched questions from industry forums, compliance communities, and risk practitioner networks spanning fraud detection services, KYC verification, KYB solutions, digital footprinting, customer risk scoring, deepfake detection, and AML compliance and answered every single one.

Whether you’re evaluating vendors, building an internal risk function, or trying to understand where your current stack has gaps, this is the reference guide the industry has been asking for.

Top 50 industry-driven questions that Atna AI experts answered

Q1. What are fraud detection services and how do they work?

Fraud detection services use AI, machine learning, and behavioral analytics to identify suspicious patterns in real-time transactions, onboarding flows, and customer behavior. Modern fraud detection solutions analyze thousands of data signals device fingerprints, IP reputation, transaction velocity, and identity mismatches to flag or block fraudulent activity before it causes financial loss.

Q2. What’s the difference between fraud detection and fraud prevention solutions?

Fraud detection identifies fraud as it happens or after the fact, while fraud prevention solutions stop it before it occurs. The most effective platforms combine both — using real-time risk scoring during onboarding and transactions, plus ongoing monitoring to catch emerging fraud patterns early.

Q3. Which industries need fraud detection services the most?

Insurance, banking, fintech, lending, and e-commerce rely most heavily on fraud detection services. Insurance fraud detection is particularly critical, with claims fraud costing the industry billions annually. Other high-need sectors include crypto exchanges, digital wallets, and regulated financial services requiring AML compliance.

Q4. How accurate are AI-powered fraud detection solutions?

Leading AI-powered fraud detection solutions achieve 95–99%+ accuracy by combining supervised ML models with real-time behavioral signals. Accuracy depends heavily on model training data, feature richness (e.g., digital footprinting, device intelligence), and how frequently the model is retrained against new fraud patterns.

Q5. What data does a fraud detection service use to flag risk?

Fraud detection services draw on identity data, device fingerprints, IP geolocation, email age and activity, phone carrier signals, behavioral biometrics, transaction history, and social graph analysis. The richer the data stack, the lower the false positive rate — meaning fewer genuine customers are incorrectly blocked.

Q6. Can fraud detection solutions work in real time?

Yes. Real-time fraud detection solutions deliver risk decisions in milliseconds via API, enabling businesses to accept, flag, or reject users and transactions at the point of action — during login, payment, account creation, or insurance claims submission — without adding friction for legitimate users.

Q7. What is the cost of fraud detection services?

Fraud detection service pricing typically follows API call volume, with enterprise plans priced on monthly active users or transaction count. Mid-market platforms range from a few hundred to several thousand dollars monthly. The ROI is typically measured against fraud losses prevented and manual review costs reduced.

Q8. How do fraud detection solutions reduce false positives?

Reducing false positives requires layered signals — not just single-point checks. The best fraud prevention solutions combine behavioral analytics, device intelligence, and risk scoring with configurable thresholds so businesses can tune sensitivity based on their risk appetite without blocking good customers.

Q9. What’s the difference between rule-based and AI-based fraud detection?

Rule-based fraud detection uses fixed logic (e.g., “flag transactions over $10,000 from new accounts”) — fast but rigid. AI-based fraud detection solutions learn continuously from patterns, adapting to new fraud tactics in ways static rules cannot. Most modern platforms use a hybrid approach.

Q10. How do fraud detection services handle new or synthetic fraud patterns?

Advanced fraud detection services use unsupervised machine learning and anomaly detection to identify never-before-seen fraud patterns — including synthetic identity fraud, where fraudsters combine real and fake data. Digital footprinting solutions play a key role here by detecting inconsistencies invisible to traditional ID checks.

Q11. Can fraud detection solutions integrate with existing systems?

Yes. Enterprise fraud detection solutions offer REST APIs and webhooks that integrate with CRMs, core banking systems, insurance platforms, and onboarding workflows. Low-code SDKs and no-code connectors (Zapier, Make) reduce integration timelines from weeks to days.

Q12. What compliance standards do fraud detection services support?

Fraud detection and AML compliance platforms typically align with GDPR, CCPA, PCI-DSS, FATF guidelines, and local financial regulations. Built-in audit trails, data residency options, and explainable AI outputs help compliance teams satisfy regulatory requirements without manual documentation overhead.

Q13. What is AML compliance and why does it matter?

AML (Anti-Money Laundering) compliance refers to the legal and operational processes financial institutions use to detect, report, and prevent money laundering. Fraud prevention and AML compliance solutions automate transaction monitoring, suspicious activity reporting (SAR), and customer risk scoring to meet regulatory obligations efficiently.

Q14. How are fraud prevention and AML compliance connected?

Fraud prevention and AML compliance overlap significantly — both require real-time risk assessment, identity verification, and behavioral monitoring. Integrated platforms that combine fraud signals with AML watchlist screening give compliance teams a unified risk picture instead of siloed tools.

Q15. What is transaction monitoring in AML compliance?

Transaction monitoring is the process of continuously reviewing financial activity to detect patterns indicative of money laundering, terrorism financing, or fraud. AML compliance platforms automate this with configurable rules and ML models that reduce manual review workloads while improving detection rates.

Q16. What triggers a suspicious activity report (SAR)?

SARs are triggered when fraud detection or AML compliance systems identify transactions or behaviors that suggest illegal activity — structuring, unusual wire transfers, high-volume cash activity, or mismatches between stated purpose and actual behavior. Automated fraud prevention solutions flag these for compliance officer review.

Q17. How does customer risk scoring work in AML?

Customer risk scoring assigns a dynamic risk tier (low/medium/high) to each customer based on identity attributes, transaction behavior, geographic exposure, PEP/sanctions status, and historical patterns. Fraud prevention and AML compliance platforms update scores continuously, triggering enhanced due diligence when risk elevates.

Q18. What is enhanced due diligence (EDD)?

Enhanced due diligence is a deeper level of customer verification required for high-risk individuals and entities. It typically includes source of funds verification, adverse media screening, and more frequent review cycles. Fraud prevention solutions automate EDD workflows for customers flagged by customer risk scoring systems.

Q19. Can small fintechs afford AML compliance solutions?

Yes. Modern AML compliance platforms offer usage-based pricing that scales with transaction volume, making them accessible to early-stage fintechs. The real cost of non-compliance — regulatory fines, license revocation, reputational damage — far exceeds the investment in a proper fraud prevention and AML compliance stack.

Q20. What’s the difference between KYC and AML compliance?

KYC (Know Your Customer) is the identity verification component — confirming who a customer is at onboarding. AML compliance is the ongoing process — monitoring behavior, screening against watchlists, and reporting suspicious activity. Both are required together; KYC verification services feed customer data into AML monitoring workflows.

Q21. How do fraud prevention solutions handle PEP and sanctions screening?

Fraud prevention and AML compliance platforms integrate with global PEP (Politically Exposed Person) and sanctions databases — OFAC, UN, EU, HM Treasury — screening customers at onboarding and on an ongoing basis. Automated alerts flag matches for manual review, with full audit trails for regulatory evidence.

Q22. What is the role of AI in AML compliance?

AI in AML compliance reduces false positive rates (which average 95%+ in rule-based systems), adapts to evolving laundering typologies, and automates case prioritization. Machine learning models trained on labeled fraud and AML data dramatically improve the signal-to-noise ratio for compliance teams.

Q23. What is KYC verification and what does it involve?

KYC (Know Your Customer) verification confirms a customer’s identity using government-issued ID, biometric checks, liveness detection, and data cross-referencing. KYC verification services are mandatory for banks, fintechs, insurers, and any regulated entity onboarding new customers.

Q24. What is a KYB solution and how does it differ from KYC?

A KYB (Know Your Business) solution verifies the identity and legitimacy of a business entity — including UBO (Ultimate Beneficial Owner) mapping, company registry checks, and adverse media screening. KYC verification services focus on individuals; KYB solutions focus on corporate clients and are essential for B2B onboarding in financial services.

Q25. How fast can KYC verification services onboard a customer?

Modern KYC verification services using automated document checks and AI-powered liveness detection can complete onboarding in under 60 seconds. End-to-end automation — from ID capture to identity match to risk scoring — eliminates manual review bottlenecks for the majority of applicants.

Q26. What is digital footprinting and how does it detect fraud?

Digital footprinting solutions analyze the passive signals left by a user’s online presence — email age, social media activity, domain registration history, phone number usage, and device behavior — to build a trust score. A thin or inconsistent digital footprint is a strong indicator of synthetic identity or first-party fraud.

Q27. How do digital footprinting solutions complement traditional KYC?

Traditional KYC verification checks documents and selfies. Digital footprinting solutions add a behavioral and reputational layer — verifying whether the identity behind the document has a credible, consistent online history. Together, they catch fraudsters who pass document checks using stolen or synthetic identities.

Q28. What is UBO mapping in a KYB solution?

UBO (Ultimate Beneficial Owner) mapping traces the ownership chain of a business entity to identify individuals who own 25%+ of shares or exercise significant control. KYB solutions automate this process using global company registries, reducing the weeks-long manual research required for complex corporate structures.

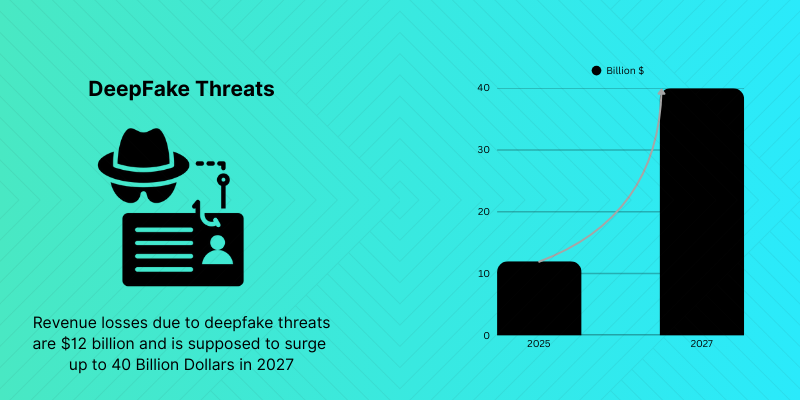

Q29. What is deepfake detection and why is it relevant to KYC?

Deepfake detection solutions identify AI-generated synthetic media — manipulated videos, voice clones, and face swaps — used to bypass liveness checks in KYC verification. As deepfake technology becomes widely accessible, deepfake detection is becoming a core requirement for any biometric-based onboarding workflow.

Q30. How do deepfake detection solutions work technically?

Deepfake detection solutions use a combination of computer vision models, liveness analysis, physiological signal detection (micro-blinking, skin texture), and metadata forensics to distinguish genuine video from AI-generated content. The best solutions are trained on continuously updated datasets of emerging deepfake methods.

Q31. What is customer risk scoring and how is it used in onboarding?

Customer risk scoring assigns a real-time risk rating to each new user based on identity signals, digital footprint, device characteristics, and behavioral patterns during onboarding. High-risk scores trigger step-up verification or manual review, while low-risk users pass through frictionlessly — balancing security and conversion.

Q32. Can KYB solutions handle international company verification?

Yes. Enterprise KYB solutions access company registries, beneficial ownership databases, and adverse media sources across 100+ countries, enabling global business onboarding. Cross-border KYB is particularly important for correspondent banking, trade finance, and global insurance platforms.

Q33. What is eKYC and how does it differ from manual KYC?

eKYC (electronic KYC) is the fully digital, automated version of identity verification — using AI document processing, biometric matching, and database cross-referencing instead of in-branch checks. eKYC verification services reduce onboarding costs by 60–80% compared to manual processes while improving compliance accuracy.

Q34. How does customer risk scoring change post-onboarding?

Customer risk scoring is dynamic — not a one-time check. Post-onboarding, scores update based on transaction behavior, watchlist changes, adverse media events, and account activity patterns. This continuous scoring enables fraud prevention solutions to flag customers whose risk profile has changed since initial KYC.

Q35. What industries use KYB solutions most?

KYB solutions are most widely used in banking (correspondent banking, SME lending), insurance (commercial underwriting), fintech (B2B payment platforms), and crypto exchanges. Any business onboarding corporate clients with AML compliance obligations needs a KYB solution.

Q36. What is insurance fraud detection and what types does it cover?

Insurance fraud detection covers claims fraud (staged accidents, inflated medical bills), application fraud (misrepresented risk), ghost brokering, and internal fraud. AI-powered insurance fraud detection solutions analyze claims data, behavioral patterns, and third-party intelligence to flag suspicious cases before payouts are made.

Q37. How does AI improve insurance fraud detection over manual review?

AI-powered insurance fraud detection processes thousands of claims variables simultaneously — inconsistencies in injury patterns, duplicate claim submissions, social media cross-referencing, and network link analysis — at a scale and speed no human team can match. This reduces claim leakage while cutting investigation costs.

Q38. What is claims fraud and how prevalent is it?

Claims fraud occurs when policyholders or third parties deliberately misrepresent or fabricate claims. Industry estimates put insurance fraud at 10–15% of total claims costs globally. Fraud detection solutions with ML scoring and network analysis are the primary defense against claims fraud at scale.

Q39. Can fraud detection solutions catch organized fraud rings?

Yes. Advanced fraud detection solutions include network graph analysis that maps relationships between claimants, providers, and intermediaries — identifying organized fraud rings that individual transaction checks miss. This is particularly powerful in auto, health, and workers’ compensation insurance fraud detection.

Q40. How do deepfakes threaten insurance and financial services fraud?

Deepfake detection is becoming critical in financial services and insurance as fraudsters use AI-generated video to impersonate customers during video KYC, create fake evidence for claims, and synthesize voice for phone-based authentication bypass. Deepfake detection solutions are now a must-have layer in any identity verification stack.

Q41. What is the ROI of implementing fraud detection solutions?

The ROI of fraud detection solutions is typically measured as fraud losses prevented minus platform costs, plus operational savings from reduced manual review. Most enterprises report 3–8x ROI within the first year, with payback periods under 6 months when fraud rates exceed 0.5% of transaction volume.

Q42. How do I evaluate fraud detection vendors?

When evaluating fraud detection services, assess: detection accuracy (true positive rate), false positive rate, API latency, coverage of your specific use case (insurance, KYC, payments), global data coverage, integration complexity, explainability of decisions, and compliance certifications. Always request a proof-of-concept on your own data.

Q43. What should I look for in a fraud prevention solution for insurance?

Look for insurance-specific fraud detection features: claims linkage analysis, medical billing pattern detection, geospatial inconsistency flagging, and integration with industry data consortia. Generic fraud prevention solutions often miss insurance-specific fraud typologies that purpose-built platforms catch by default.

Q44. How long does it take to integrate a fraud detection API?

Most modern fraud detection APIs offer REST endpoints with well-documented SDKs, enabling basic integration in 1–3 days. Full production deployment — including custom risk threshold configuration, webhook setup, and dashboard training — typically takes 2–4 weeks for enterprise environments.

Q45. What is payment fraud detection and how does it differ from identity fraud?

Payment fraud detection focuses on transaction-level anomalies — unusual amounts, mismatched geolocation, velocity abuse, and card-not-present fraud. Identity fraud detection focuses on who is transacting. The best fraud detection solutions combine both layers, linking identity risk signals to payment behavior for holistic protection.

Q46. How do fraud prevention solutions scale with business growth?

Cloud-native fraud detection services scale horizontally — handling millions of API calls per day without performance degradation. Usage-based pricing models mean costs scale proportionally with volume, and ML models improve in accuracy as they process more customer data over time.

Q47. What is the difference between fraud detection and risk scoring?

Fraud detection is binary — flagging specific events as fraudulent. Customer risk scoring is continuous — assigning a dynamic probability of fraud risk to users and transactions. Risk scoring feeds into fraud detection workflows, enabling tiered responses (approve, step-up verify, decline) rather than binary block/pass decisions.

Q48. How do fraud detection solutions handle GDPR and data privacy?

GDPR-compliant fraud detection services process only the minimum necessary personal data, provide data subject access and deletion mechanisms, and maintain lawful basis for processing (legitimate interest for fraud prevention). Look for solutions with EU data residency options and ISO 27001 certification.

Q49. What is the future of fraud detection technology?

The future of fraud detection solutions includes federated learning (training models across datasets without sharing raw data), large language model-based anomaly detection, real-time biometric continuous authentication, and cross-industry fraud consortia sharing signals. Deepfake detection solutions and digital footprinting will become baseline requirements across all regulated industries.

Q50. Why is digital footprinting becoming essential in fraud prevention?

As document fraud becomes easier with AI tools, digital footprinting solutions provide a fraud signal that is far harder to fake — a coherent, long-standing online presence. Fraudsters can produce synthetic IDs but cannot fabricate years of consistent digital behavior across email, social, device, and network signals. This makes digital footprinting one of the highest-signal inputs in modern customer risk scoring.

Conclusion

The questions in this guide reflect where the industry is right now: moving from reactive, rules-based fraud detection toward proactive, AI-powered fraud prevention solutions that combine identity intelligence, behavioral signals, and real-time risk scoring into a single, explainable decision layer.

What’s clear from these 50 questions is that no single tool is enough. Effective fraud prevention requires KYC verification services that go beyond document checks, KYB solutions that unravel complex ownership structures, digital footprinting solutions that surface signals traditional ID checks miss, deepfake detection that keeps biometric onboarding honest, and AML compliance workflows that turn raw data into defensible regulatory evidence.

The organizations winning against fraud today aren’t the ones with the biggest teams they’re the ones with the most connected intelligence. The right fraud detection services don’t just block bad actors; they do it without slowing down the good ones.

If these questions reflect the challenges your team is navigating, the answers don’t have to stay theoretical. The technology to solve them exists and it’s more accessible than most compliance and risk teams realize.

01

How can AI improve fraud detection accuracy in financial institutions?

+

AI analyzes large volumes of transactions in real time to identify suspicious patterns. This helps organizations detect fraud faster and reduce false positives.

02

What are the biggest challenges in modern fraud prevention?

+

Evolving fraud tactics, increasing transaction volumes, and manual review limitations are key challenges. Organizations need adaptive, AI-driven systems to stay ahead of emerging threats.

03

Can AI help reduce false positives in fraud monitoring?

+

AI uses behavioral analysis and contextual data to make more accurate decisions. This minimizes unnecessary alerts and improves investigation efficiency.

04

How does real-time transaction monitoring help prevent fraud?

+

Real-time monitoring identifies suspicious activities as they occur rather than after the fact. This enables faster intervention and reduces potential financial losses.

05

Why is explainable AI important in fraud detection?

+

Explainable AI provides clear reasons behind fraud risk scores and alerts. This improves trust, supports compliance requirements, and aids investigation teams.