Claims were once highly document-driven. Every process workflow in an insurance company depends upon the documents that they collect from the insurer. Before the AI era, what seemed flawless has now become a highly risk-prone area.

The rise of document deepfakes has changed the narrative. Once a controlled and streamlined process, it has now become a high-risk-prone area in the insurance sector. The influencers are unstructured data and deepfake-driven document fraud.

These two factors pose a serious operational hindrance. Any organization that runs its revenue on such documents is running towards implementing a robust TrustOps architecture to combat deepfake document fraud. The deepfake impact is higher, reaching losses in the hundreds of billions, as UNESCO took to quote.

“We are approaching a synthetic reality threshold—a point beyond which humans can no longer distinguish authentic from fabricated media without technological assistance.”

Slower claims and process interruptions are draining the revenue, leaving organizations no time for a breather. This blog highlights the structural impact of claims, increasing disputes, and quietly draining revenue. For insurance leaders, these are no longer back-office issues; they are enterprise-level concerns that directly affect profitability and trust.

The Two Big Setbacks for Insurance: Unstructured Data and Deepfakes

Documentation is what insurance is all about. Claims are made based on the validity, wholeness, and truth of documents provided by policyholders and third parties. Nevertheless, the vast majority of these documents come in unstructured forms in PDFs, scanned images, handwritten notations, emails, and photographs.

Meanwhile, recent generative AI developments have enabled creating more convincing-looking documents than ever before that can pass across records and evade conventional verification. Fake medical records, AI-generated bills, and forged identity papers are no longer a case of edge cases; it is now being incorporated into the spectrum of fraud schemes.

What has been achieved is a claims environment in which there has been an increase in volume, a decrease in clarity, and a multiplied risk.

The Growing Burden of Claim Documentation

One insurance claim may include dozens of documents that are provided in the course of time by various sources. It is projected that claims teams should be able to read, interpret, validate, and correlate all of them and make a decision.

This paper-bound system is cumbersome at every level:

- Claims handlers take a longer period of time examining documents than assessing risk.

- Critical information is overlooked because of exhaustion or lack of uniformity.

- Cross-document discrepancies are not easy to notice.

- The indicators of fraud are concealed in document noise.

This burden cannot be taken with the increasing claim volumes. Expanding operations without looking into the complexity of documents will only increase the inefficiency.

The Impact on Insurance Firms

1. Unstructured Data Leads to Longer Claim Cycles

Systems are unable to analyze unstructured documents. Human interpretation renders slow claim processing and inconsistency

This leads to:

- Extended turnaround times

- Greater front and back with customers.

- Increased costs of operation on a case-by-case basis.

- Reduced customer satisfaction.

What is perceived to be a service delay is actually a data problem.

2. Deepfake Claims Trigger Costly Appeals and Disputes

Deepfake document fraud can easily get through first assessments, only to be doubted at a later stage when it comes to audits, investigations, or after-settlement evaluations. Insurers are subjected to:

- Costly claim reversals

- Legal disputes and appeals

- Regulatory scrutiny

- Reputational damage

In most instances, the responsibility of proving fraudulent claims is transferred to the insurers, even in situations where the challenge is made, which increases the legal and administrative expenses.

The Numbers Behind the Risk

The industry research has projected that 5-10 percent of insurance claims have some aspect of fraud, with the most popular one being the manipulation of documents. The processing cost of claims may take up to 15% of the total value of claims, at least half of which is because of manual document processing.

Worse still, the cost is not visible, which is fraud that cannot be easily detected due to the inability of systems to make sense out of and verify the unstructured documents. Such losses do not manifest themselves in fraud line items; they manifest themselves in high loss ratios and operational inefficiencies.

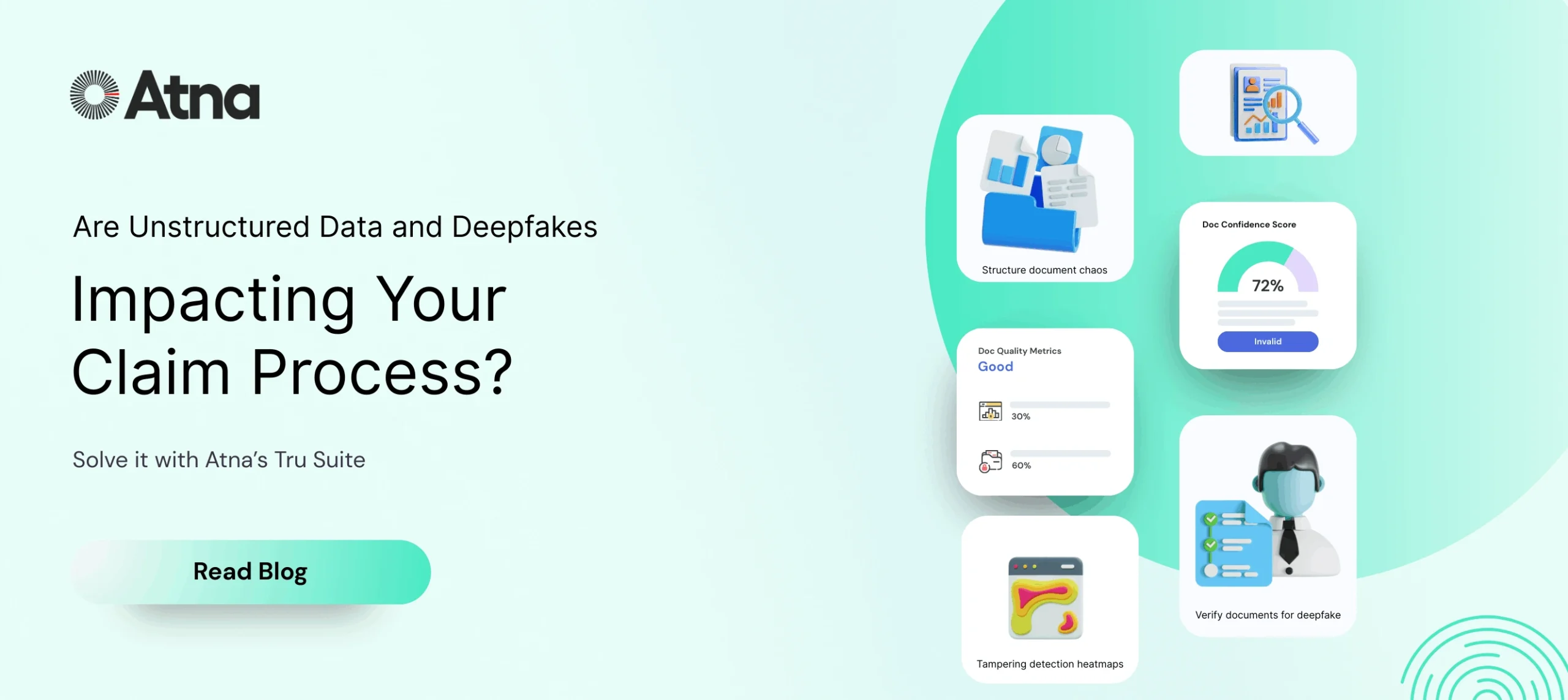

The Atna Solution

Atna is trying to solve this issue of deepfake document fraud by reconsidering the manner in which claims documents are processed in the first place.

Atna allows insurers, through the Tru Series to:

- Check the certificates of the documents submitted.

- Digitize unstructured documents into structured and analysis-ready data.

- View correlate information of all claim documents simultaneously.

- Early surface anomalies, inconsistencies, and indications of fraud.

Atna is not a document treatment but instead a conversion of documents into actionable intelligence to enable claims teams to use it as an instinctive means of information and not as a means of document interpretation.

Protect Your Revenue Before It Leaks

The insurance cannot always lose revenue through big, high-profile frauds. It spurts silently more frequently, in the form of stagnant decision-making, invisible deepfakes, and claims management that is not very efficient.

Insurers can:

- Reduce claim leakage

- Shorten settlement cycles

- Enhance the level of fraud detection.

- Operation on a scale and no proportional increase in costs.

- It does not mean adding friction; it means adding clarity.

Conclusion

There are no longer emergent risks like unstructured documents and deepfakes, but active interferences in the insurance claims process. Those organizations that still stick to manual reviews and disjointed checks will learn to control losses and preserve trust with even greater difficulty.

The future of claims is document intelligence – in which authenticity is assured, documents are organized, and decisions are suitably confident. To insurers, this cannot be a mere operation upgrading but they need to do it since it is a strategic requirement.

Leave a Reply